Beyond Carnaval: The Gov Inaugurated Brazilian VC

Beyond Carnaval: The Gov Inaugurated Brazilian VC

Concise reflections, digests, and highlights of the week's significant news within Brazil's investment and innovation landscape.

Welcome to I'm No Economist

I'm No Economist is a newsletter dedicated to deciphering Brazilian potential for global investment. Subscribe below to read it every week.

IN TODAY'S BEYOND CARNAVAL:

VC Is a Post-War Innovation

How the Government Played VC In Brazil

Pivotal Private Firms In Brazil

In a previous article here at I'm No Economist, "Beyond Carnaval: Govs Also Drive Change", the spotlight was placed on the (often-overlooked) role of government in innovation:

Yes, while tech giants and private-sector disruptors often steal the light, Nat Vasconcellos wrote about how governments, through policy, investment, and infrastructure, are foundational to technological progress.

Globally, these markets have become essential pillars for innovation, and in Brazil, VC has evolved into a critical driver of entrepreneurship, taking its place alongside government-backed initiatives. But how did it start in Brazil?

I'm a sucker for history and biographies. This article will have a little bit of that too. Hope you like it. Let's dive into it.

Venture Capital: A Post-War Innovation

AI helped with research

Americans would say the VC industry was born in the 1800s with the whale hunting market being its predecessor. Probably because American independence happened only a few decades before that, they can't relate to the 1500s' great navigation period. But that's neither here nor there.

The fact is that Venture capital (VC) is a post-World War II innovation. And the industry has gone through a lot of transformation in the United States since its inception in the 1940s.

In 1946, Georges Doriot, a French-born professor at Harvard Business School, founded the American Research and Development Corporation (ARDC or ARD as sometimes seen in literature), one of the first VC firms. Doriot's vision was to fund innovative, real long-shot tech companies, leading to significant investments in early technology companies. The most notable case was Digital Equipment Corporation (DEC) in 1957 which received $2Mn in venture debt and $70,000 in equity - that company was acquired by Compaq by the end of the 1990s.

It was pretty much boring compared to the complex framework VCs have nowadays until the 1970s, a year that marked a pivotal shift as institutional investors began to enter the venture capital landscape. The creation of the Employee Retirement Income Security Act (ERISA) in 1974 which proposed a more transparent governance for private capital managers to report results.

Firms like Kleiner Perkins and Sequoia Capital emerged during this time, focusing on technology startups in Silicon Valley. Here's where conventional wisdom says that VC was inaugurated as we know it today. Eugene Kleiner was one of the traitorous eight who left a competitor to found Fairchild Semiconductor - watch out Jansen Huang.

Then, the 1990s were characterized by a significant growth due to the internet boom. Venture capital funding surged as firms sought to capitalize on the burgeoning tech sector. Notable firms such as Benchmark Capital and Accel Partners gained prominence by investing in internet startups like eBay and Amazon.

Following the dot-com crash, venture capital experienced a recovery phase characterized by diversification into new sectors beyond technology, including healthcare and clean energy. The 2010s were then dominated by tech giants like Facebook, Google, and Uber, which attracted massive VC funding rounds for the app revolution. The total amount of VC investment reached new heights, with firms like Andreessen Horowitz raising significant funds to back high-growth startups.

Today, VC is a $320Bn asset class globally (dry powder). This goes to show how important this kind of investment is for intelligent people to take advantage of to build for the future.

How The Government Played VC In Brazil

One of the most notable cases of the right use of BNDES funds was Microsiga (today, the company is known as TOTVS). By the way, we have to finish telling that story

.In the late 1990s, Microsiga, a Brazilian software company founded in 1983 by Laércio Cosentino and Ernesto Haberkorn was emerging as a leader in enterprise resource planning (ERP) software for small and medium-sized enterprises (SMEs).

At that time, Brazil’s tech landscape was still underdeveloped, and few companies had the resources or access to capital to scale. Recognizing the potential of Microsiga and the broader tech industry, BNDESPAR, the equity arm of BNDES, took a strategic stake in the company:

"In February of 2005, TOTVS had its D-Day. What they did was a master play only fit for a select few. The kind of deal-making done is worthy of an award, if they gave one.

In 24 hours the company bought back the shares of Advent Internacional, acquired one of its main competitors, Logocenter, and welcomed a new investor.

The first transaction that made Microsiga's revenue grow by 25%, was the purchase of Logocenter.

This set the ground for a new transaction that very day, which was getting funding from the Brazilian Development Bank (BNDES). They received R$ 40 million for 17,6% that day, making BNDES a shareholder of the company.” Read more here

The BNDES investment was critical because it provided the capital needed for Microsiga to expand its operations and innovate its product offerings, eventually becoming one of the largest software firms in Latin America.

The investment also signaled the Brazilian government’s commitment to fostering the tech sector as a vital part of economic modernization.

Pivotal Private Firms In Brazil

When it comes to private capital, firms like Advent International and Silver Lake were the most notable investors in growth-stage companies such as TOTVS and Locaweb, a family business turned unicorn. But these are Private Equity firms. There were little to no VC firms in Brazil until the 2000s.

Brazil’s entry into the global VC scene began in the early 2000s. Local firms such as Monashees began placing early bets on Brazil’s nascent tech startups. Despite the country’s challenging regulatory environment and bureaucracy, these firms saw opportunities, especially in sectors such as e-commerce and fintech, where gaps in the market were wide.

But the 2010s saw a dramatic acceleration in Brazil’s VC market, coinciding with broader global interest in Latin America as a whole. This period is when we see the rise of some of Brazil’s biggest tech successes, such as Nubank and 99, as the country became Latin America’s largest recipient of venture capital.

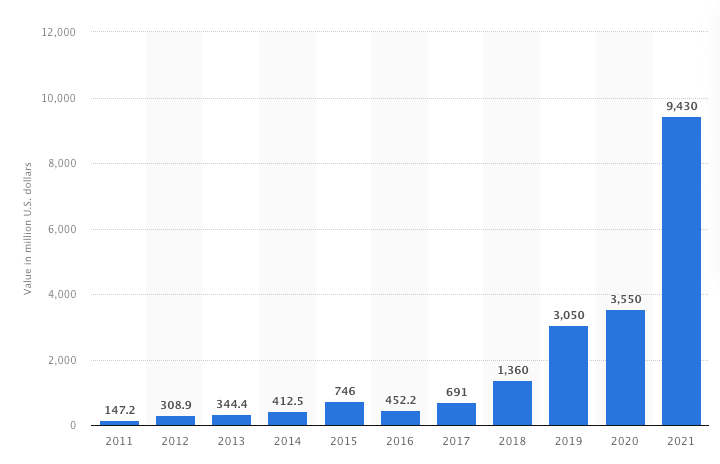

In 2021 alone, during the global startup boom, Brazilian startups raised over $10 billion in VC funding, driven by industries like fintech, e-commerce, and SaaS. Global firms like SoftBank and Sequoia have since entered the market, while local players like Monashees and Kaszek Ventures have become major investors, supporting companies like Nubank and 99. This marks a dramatic shift in Brazil’s role in the global VC landscape.

Brazilian regulatory bodies, such as the Central Bank, played a role in fostering innovation, introducing policies like open banking, which catalyzed the growth of fintech.

What really changed the game, though, was a ZIRP environment in the early 2020s that skewed the numbers for funds raised by both asset managers and startups. This triggered interest from foreign investors, who began to see Brazil not only as a potential market but also as a breeding ground for tech-driven startups.

At the same time, Brazil’s growing internet penetration, which stood at over 80% by 2023, and the rapid adoption of smartphones, have created fertile ground for e-commerce, fintech, and SaaS companies.

As we can see, the VC market in Brazil remained relatively underdeveloped until the 2010s, largely due to macroeconomic instability and a weak entrepreneurial ecosystem for disruptive tech.

However, with improving economic conditions (since the 1980s, not since 2021) and a thriving tech scene, Brazil emerged as Latin America’s largest VC market. Brazil still gets most of the funding due to its continental nature and entrepreneurial background.

Brazilians are entrepreneurial people, but the culture and education to form STEM professionals is still incipient. There's a long road to go, but I'm more and more convinced we're walking in the right direction. At least there's increasing awareness. One can hope and work for it - IANE is doing its part.

Who else is?

Luis Stuhlberger is implementing cuts and restructuring Verde Asset Management, Brazil’s largest hedge fund. The changes include reducing the team and altering investment strategies to better navigate challenging economic conditions, aiming to improve the firm’s performance and agility in an uncertain market environment. (Source)

Versi raised R$50 million via a Certificate of Real Estate Receivables (CRI) to boost Brazil’s affordable housing program, Minha Casa Minha Vida. This funding will help expand the availability of homes for low-income families, addressing Brazil’s housing deficit. (Source)

Brazilian venture capitalists need R$400 billion in exits through mergers, acquisitions, or IPOs to sustain returns. The limited exit opportunities are creating a backlog in the investment cycle, challenging the sustainability and growth of Brazil’s VC ecosystem. (Source)

📩 Partner with I'm No Economist

Deciphering Brazilian potential. Generating expert intelligence and strategic insights for the Brazilian investment market.

Every Thursday 06:09 am (BR time), the Beyond Carnaval newsletter offers concise reflections, digests, and highlights of the week's significant news within Brazil's investment and innovation landscape.

Delivered on the first Saturday of the month at 06:09 am (BR time), the Open Zeitgeist newsletter provides a space for both Brazilian and "gringo" guests to share their perspectives on Brazilian investment opportunities.

Investors are closely looking for opportunities in our country. It is our job to decipher Brazilian potential.