I'm No Economist #11: 🪙 How Has Election Affected The Brazilian Economy?

Take no advice from me. I'm No Economist

I don't follow elections too closely. I don't have a party representing me, and I don't believe a single candidate can catalyze any significant change (for the best) in just a couple of mandates. Politics haven't changed much since the pre-republic 1850s. Why will an election change anything now?

Although the strongest GDP in Latam, and despite being one of the most sought-after markets for innovation and risk capital investments, Brazil is still just a spectator of bigger, more developed, and faster-growing nations around the world.

As a stoic, when it comes to macroeconomics, I can only prepare for the worst and adjust my portfolio and investment decisions accordingly.

And since it's been a lot of speculation about the country's economic prowess, for this edition I wanted to bring some clarity over macroeconomics.

In I'm No Economist #11 you'll read a quick digest on:

Brazil's fiscal dominance;

Brazil's external debt levels;

Brazil's current foreign exchanges reserves levels;

And the current sentiment of the investors towards Brazil.

Spoiler: you'll probably see how much the president's choice may not matter much after all.

Welcome to another edition of I'm No Economist 🎉

I'm No Economist is one of the best ways to get news - mostly opinions - on investment strategies, report digests, VC, startups, innovation, and macroeconomics.

If you are as opinionated as I am and if you know people just like us, share I'm No Economist with them. Let's all be opinionated together.

Parallels: Money Week is repeating history

It's cute - and kind of sad - to see people fall for the same narrative, not even a generation past after the last time it happened.

I was in 9th grade, just an innocent 13-year-old boy, but I remember well my history & geography teachers saying how much Brazil would take off based on this cover of The Economist (you don't have a paywall in I'm NO Economist):

I bringing this up as it appears we came to a full circle. Money Week released its latest edition of "Bet on Brazil”, peddling the idea of recently re-elected president Luiz Inácio Lula da Silva as a much-needed oxygen to environmental policies, domestic investments, and the general nation's sentiment for optimistic years to come:

When I saw that, I reflected on what would be the most interesting topics to discuss regarding Brazil's development in the next couple of years, and the scenario the new old president would have to deal with.

And as many as they are, I tried to focus on Brazil's participation in the global market and how it interacts with its counterparts.

After all, Brazil is not an isolated island and many markets depend on it, as it depends on foreign trade to keep the lights on. Not literally. Ok, maybe literally.

While I believe Lula is not an absolute imbecile, it's hard to fathom the idea of him saving Brazil from its very complicated debt-to-GDP situation, fighting inflation with only interest rates rise and making sure Brazil is interesting enough to foreign investors.

Brazil's current economic challenges

Fiscal dominance

When you control the reserve currency of the world, anything's possible. That is not the case for Brazil. Mind that I said, "possible” not “advisable”.

For a country like the U.S., if they want to stimulate riskier investments and increase consumption, they can decrease interest rates almost to zero and make money virtually free. Well, you've seen it for the last decade. We gave it a couple of years and saw ✨magic✨ happen.

The opposite is also quite simple. Making a quantitative tightening by sucking currency out of the system and lowering inflation by disincentivizing demand, is a painful but rather uncomplicated thing to do. That we don't see in a while. Wonder how it'll be.

Countries that feel compelled to dance to the global macroeconomic trends can do the same. Brazil, by the way, was way faster in making a quantitative tightening. History taught us well how to react to high inflation levels.

And yes, this is where Brazil is right when it comes to macroeconomics. The U.S. and Brazil are increasing their interest rates to make sure we fight inflation quickly, and it's using the right instruments to do so.

The thing is that when the U.S. makes more dollars available, as it is a very sought-after currency, it creates smaller problems for the U.S. issuing these happiness coupons. Many countries will buy those dollars and create USD reserves.

The problem is that, for Brazil, and more so for the Brazilian currency, the Real (BRL), making it more available only makes domestic users want that currency. It hardly moves any indicator for foreign investments.

It actually creates other problems, such as making foreign investors nervous about Brazil paying its debt, both domestic and external.

That is fiscal dominance. When monetary policies alone won't do the job. And, as a consequence, makes Brazil purchase more dollars. Which in turn, makes the BRL weaker.

The country is trying really hard to fight that reality. But by looking at the numbers, I feel that is going to be difficult to revert to the reality that the BRL is going to face a bumpy road in the next few quarters. This will make a new power sweat and fight for approval in the mid-term elections in 2024.

Let's discuss the numbers I'm looking at to see why I think it's distressing for Brazil to keep following the same monetary policy it is right now:

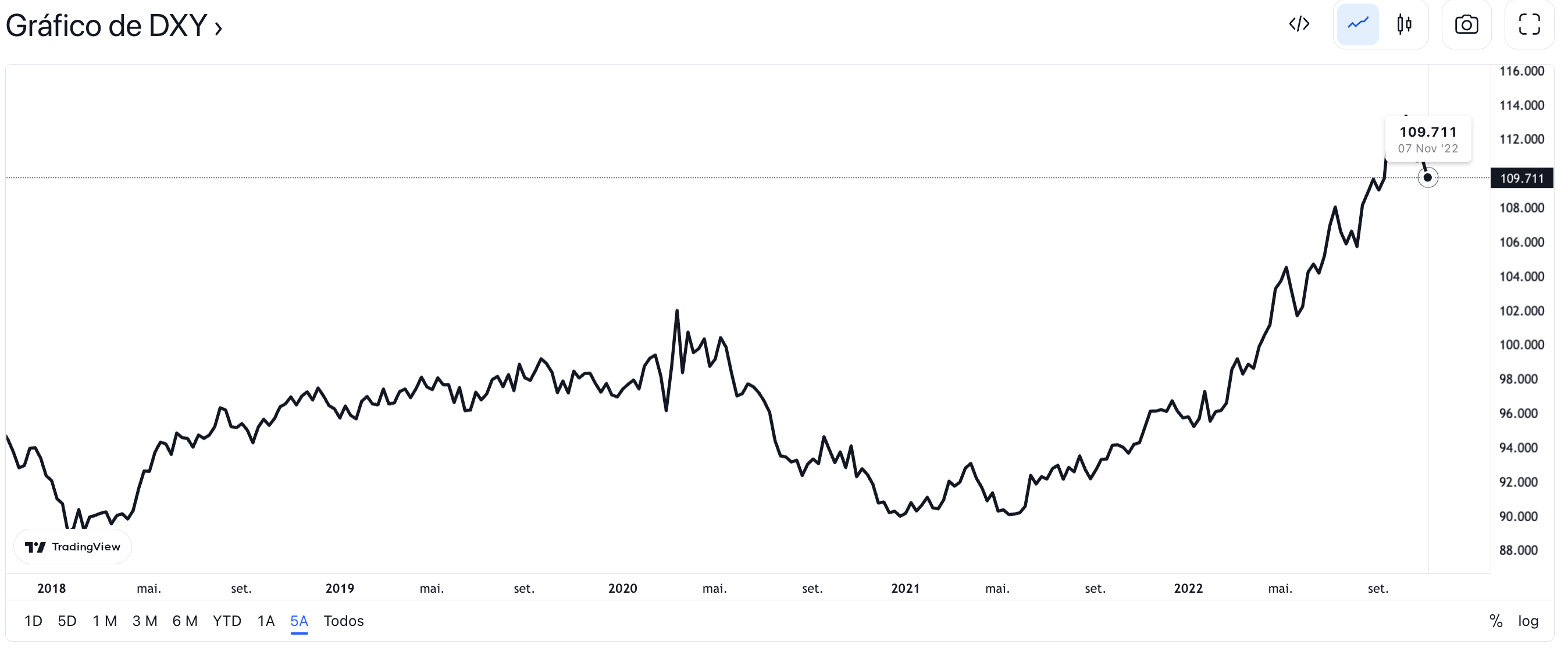

US Dollar Index (DXY)

Before explaining the domestic scenario, let me bring a few figures to show how hot is the USD compared to stronger currencies than the BRL right now.

The DXY is an index of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners' currencies. The Index goes up when the U.S. dollar gains "strength" (value) when compared to other currencies.

Here are the currencies and their weights on the DXY:

Euro (EUR), 57.6% weight

Japanese yen (JPY), 13.6% weight

Pound sterling (GBP), 11.9% weight

Canadian dollar (CAD), 9.1% weight

Swedish krona (SEK), 4.2% weight

Swiss franc (CHF), 3.6% weight

A high DXY means that the demand for the dollar, especially for its strong peer currencies, is increasingly preoccupying for the countries that have a low USD reserve.

Turns out the DXY is reaching its all-time high (ATH).

Developing countries such as Brazil will have to fight for their lives on the bread line if they want to pay for their external debt.

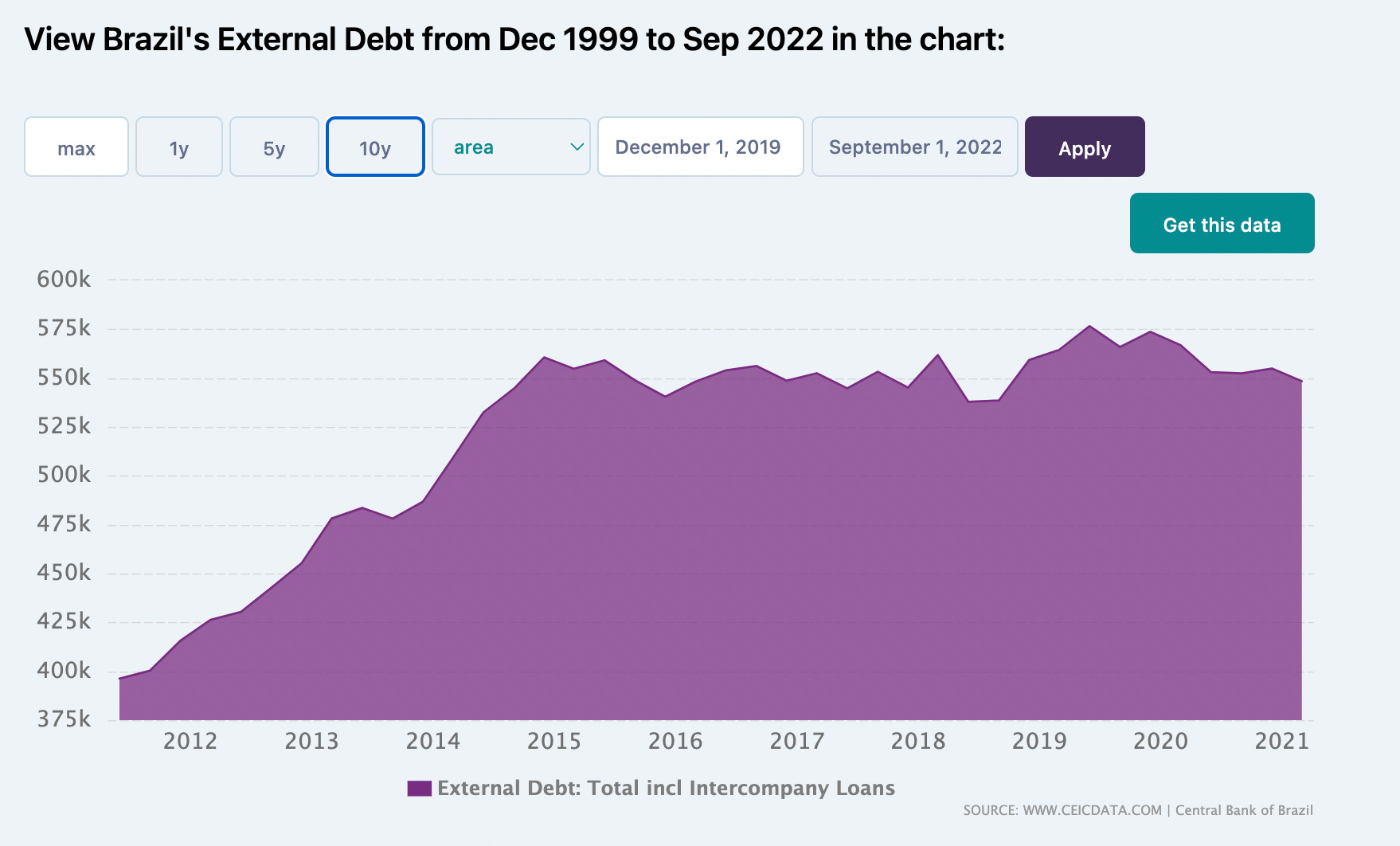

Brazil's Debt-to-GDP & External Debt

Brazil's debt-to-GDP is around 80%. Increasing interest rates to the current levels (13.75% by the time of this newsletter) makes it more and more difficult for the country to pay its debt.

It would already be a problem not to have a USD scarcity across all markets. But if it weren't for the increasing external debt Brazil has gotten into in the last 20 years, it would at least be a smaller issue.

Now help me answer this question: how is the country paying for its external debt without the most sought-after currency in the world?

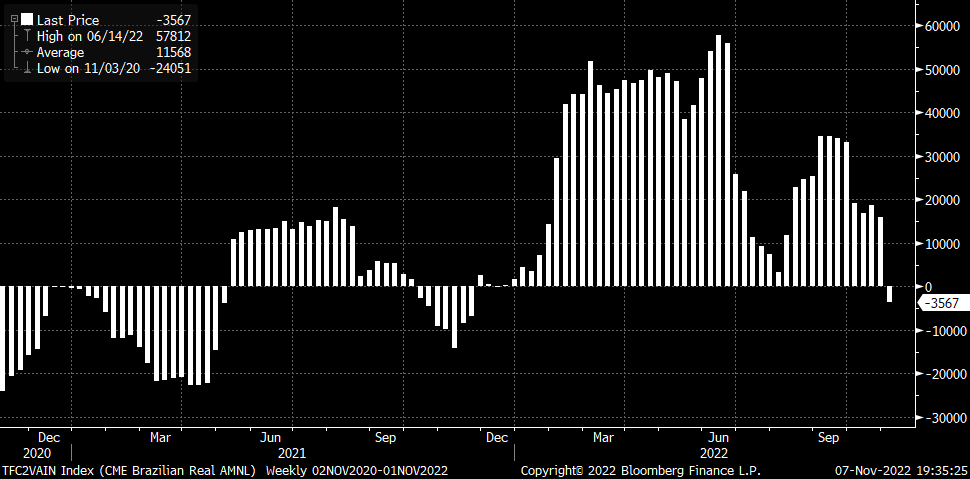

Brazil's foreign exchange reserves

Yes, compared to 20 years ago, when the foreign exchange reserves didn't even reach $100B, Brazil is at satisfactory levels. But it's impossible not to see that the recent ~15% decrease calls for some attention at this special point in history.

Especially since the CME (Chicago Mercantile Exchange) is seeing a short position in BRL for the first time in the last year, showing discredit from foreign investors in the Brazilian currency.

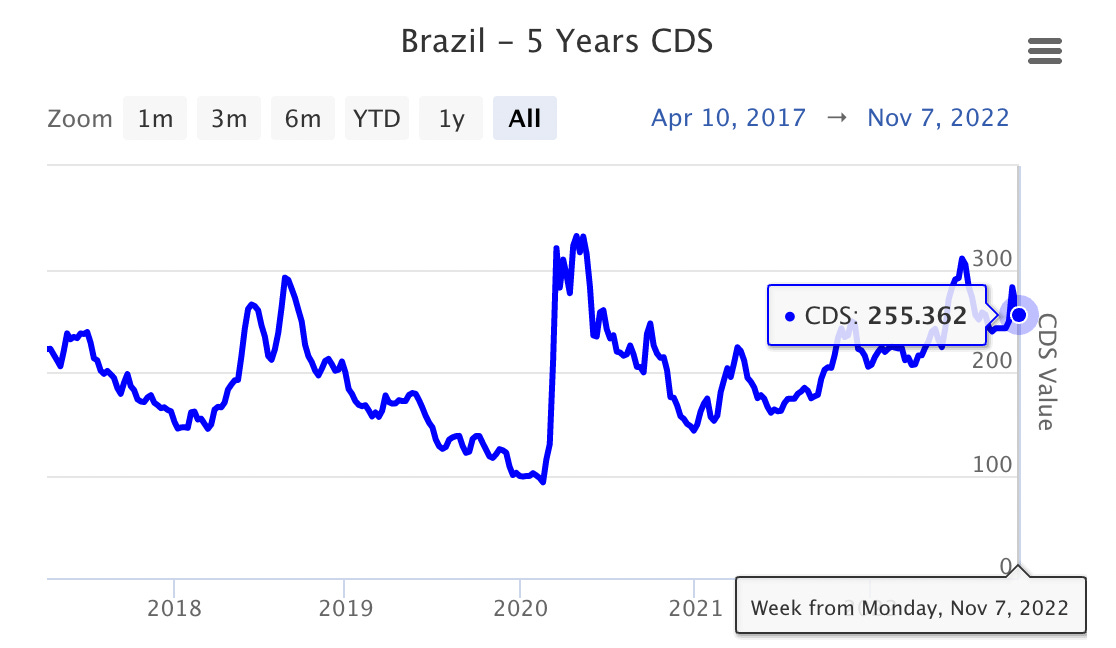

Brazil's Credit Default Swaps

It may be just a non-causation correlation. But looking at the Credit Default Swaps on the Brazilian sovereign debt, we can see how investors are reacting to the risk of investing in Brazil.

This is an important metric to monitor when it comes to the risk of default on a country's sovereign debt. In a nutshell, it's the insurance investors pay against the risk of a country defaulting on its sovereign debt.

Although now we're seeing a calmer environment than at the end of October 2022, it is becoming direr and direr, reaching pre-pandemic levels.

What will happen next?

Well, only god and Nancy Pelosi know what will happen next.

But, these are all problems that come from before the elections and have been around for more time than any of the most recent political turmoil.

I would say that anything announced in the news going forward is pure speculation and nothing more than a sentiment analysis - not a technical one.

I'm saying that reflecting on the recent short-term USD/BRL oscillation, where we almost saw the exchange rate going below 5 BRL.

But I wouldn't be surprised if we reached a new all-time high for USD/BRL in the next months.

Subscribe to I'm No Economist 📊

If you liked this content and want to stay informed with easy-to-digest content, make sure to subscribe to the newsletter!

Talk soon,

L.