I'm No Economist #5: 🗝 UBS Global Family Office Report 2022 - I Read It So You Don't Have To

Take no advice from me. I'm No Economist.

Welcome to another edition of I'm No Economist.

I'm No Economist is one of the best ways to get news - and opinions - on the 🇧🇷 and 🇺🇸 markets, startups, and the innovation ecosystem.

I promise that I have little no conflict of interest in the things I post.

If you haven't yet seen what happened previously, make sure to take a peek at the past edition and share it with your friends:

🗝 UBS Global Family Office Report 2022

At the beginning of the month of June 2022, UBS released its annual Global Family Office Report, and I read it so you don't have to.

That said, this is one of the most comprehensive reports I've read lately. If you're a nerd like myself, I advise you to at least skim through it. I'm sure you'll enjoy it.

UBS surveyed 221 Family Offices (FOs) around the world, with a collective wealth of USD 443 bn.

This is an extensive report on how family offices are thinking about their asset allocation and planning their cost structure.

TL;DR:

Asset allocation: family offices are reviewing their strategies due to high inflation and the rise of interest rates - surprise, surprise;

Private equity: this asset class is one to become the favorite among all others for higher returns. Tech may be the one taking the lightest blow among sectors.

Impact investing: due diligence will intensify to avoid "greenwashing” investments. Exclusion will still remain the most common tool. Is this an opportunity to innovate in ESG?

Digital assets and crypto: family offices in the US are more prone to investing than Asia-Pacific FOs. This investment allocation is more focused on learning how decentralized payments work than on high expectations of high returns. - yeah, right. Nobody's responsible for the Web3 pump and dump anymore.

Asset allocation

It's super fun to see how strategic asset allocation (SAA) happens. How the decision-making is designed around concerns and trying to predict the future. I love how we, as a society, managed to develop systems and methods in such a mathematical manner to make them less unpredictable.

We try to rationalize a lot of sentiments. Fear, uncertainty, doubts, aspirations, desires. I have mixed feelings about how we're doing.

FOs in this report, for instance, show different levels of those sentiments to make their asset allocation. What called my attention is that those sentiments are mainly based on their cultural context. When taking inflation into consideration, LATAM and US are quite different:

What is common between them, though, is that in times of high inflation and central banks signaling for higher rates, family offices are sacrificing their liquidity for higher returns. Fixed income allocation is due to take a hit and private markets may be the asset class benefitting from this new scenario.

FOs are also factoring in the geopolitical uncertainty in their decision-making process, which is smart.

I've been reading a bit about distressed debt investment opportunities and I'm amused to see it's really a trend in times of crisis. If FOs are fine with sacrificing liquidity over higher returns, this increase from 2019 to 2021 shows they're putting their money where their mouth is.

I'm intrigued by the decrease in deflationary assets such as real estate, precious metals, and commodities. These asset classes were divested due to the necessity for an investment increase in private equity.

Private equity

With the difficulty of finding opportunities in fixed income and public equities, especially because the number of IPOs in the US went from 280 in the year 2000 to 165 in 2020, this asset class has become the favorite for FOs.

“In the US, the world’s biggest and most diverse private equity market, the number of private equity-backed companies has grown from 1,698 in 2000 to 8,892 in 2020."

FOs tend to invest both directly into private companies and private equity funds. This is an interesting way to generate alpha while diversifying their portfolio.

The expectations for this asset class are high, and it's getting more and more competitive to get consistent returns at reasonable valuations. That's why family offices are going down the funnel to invest in earlier-stage companies and making a name for venture capital as a type of investment.

This is definitely great news for both founders and VC managers that can expect a surge in investments from FOs in 2022 and the next years to come.

When analyzing a direct investment, FOs look at tech as their preferred sector, with 82% of FOs currently investing. Healthcare and Social Assistance is the second most common, with 60% of FOs currently investing.

Impact investing

FOs, unlike other institutional investors, have greater freedom when it comes to taking their own approach toward impact investing. The report says that most investors will not change their approach to their impact investing for the next five years.

“[…] family offices aren’t fully embracing the latest developments in sustainable investing yet. The straightforward approach of excluding industries or controversial business activities is still used by many, although the European Union’s Sustainable Finance Disclosure Regime that is taking a lead on defining sustainable investing aims to steer away from pure exclusions into broader ESG integration."

Nothing will really change here. Is this a sign for VCs, startups - and innovation in general - to work on attention-worthy ESG projects?

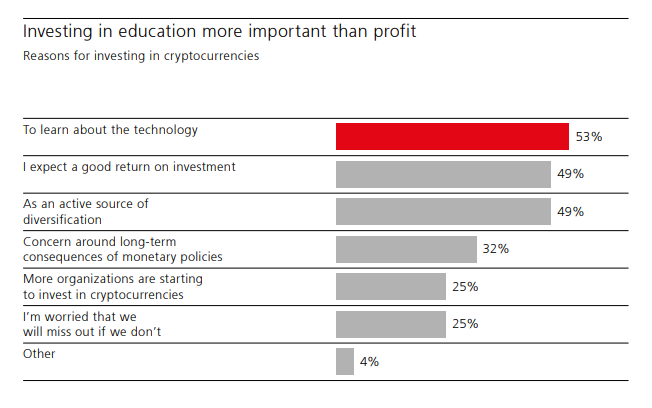

Digital assets and crypto:

Now that we're entering a crypto winter, it's hard to talk about the most volatile asset class on the planet and how you were invested in it. Family offices report that this asset class is purely for learning purposes.

However, their allocation seems to be higher (up to 3%) than other asset classes that have survived the action of time such as gold and precious metals (1%).

The report deep dives into the reasons why FOs are investing in digital assets, distributed ledger tech (DLT), and other crypto assets, and there are a lot of doubts about this asset class.

Something that never ceases to amaze me is how FOMO is an incredible trigger for people of all ages, cultures, and creeds. 25% of FOs responded that “I'm worried that we will miss out if we don't [invest]” is a reason for their allocation in this type of investment.

I'm No Economist is now on Twitter

I'm No Economist is getting serious, huh?!

We're now on Twitter so you can get the digest of the editions of the newsletters posted here.

Here's the thread I posted recently talking about how software ate the world but already spat it out:

Talk soon,

L.